Is Audit u/s 44AB required if turnover is less than one crore and profit is less than 6%/8% for FY 2017-18.

I am a salaried person and I am also engaged in F&O trading. My Gross total income is 5 Lakhs. Turnover of F&O trading is Rs. 20 Lakhs but my profit from F&O is less than 6% of turnover. I have earned only 50000/- from F&O in FY 2017-18.

Can I declare profit less than 6%?

Do I need to go for tax audit to declare profit less than limit specified in 44AD.

Please reply

Dear Ashish,

If your turnover is less than Rs. 1 crore and your profit is less than 6%/8% of your turnover for FY 2017-18 then-

- If you have filed return for FY 2016-17 under presumptive taxation scheme u/s 44AD, then you are required to go for audit for FY 2017-18 as per requirement of section 44AD(5) and 44AB(e).

- If you did not opt for 44AD in FY 2016-17 then you are not required to go for audit for FY 2017-18, even if your profit is less than limit specified in 44AD i.e. 6%/8%.

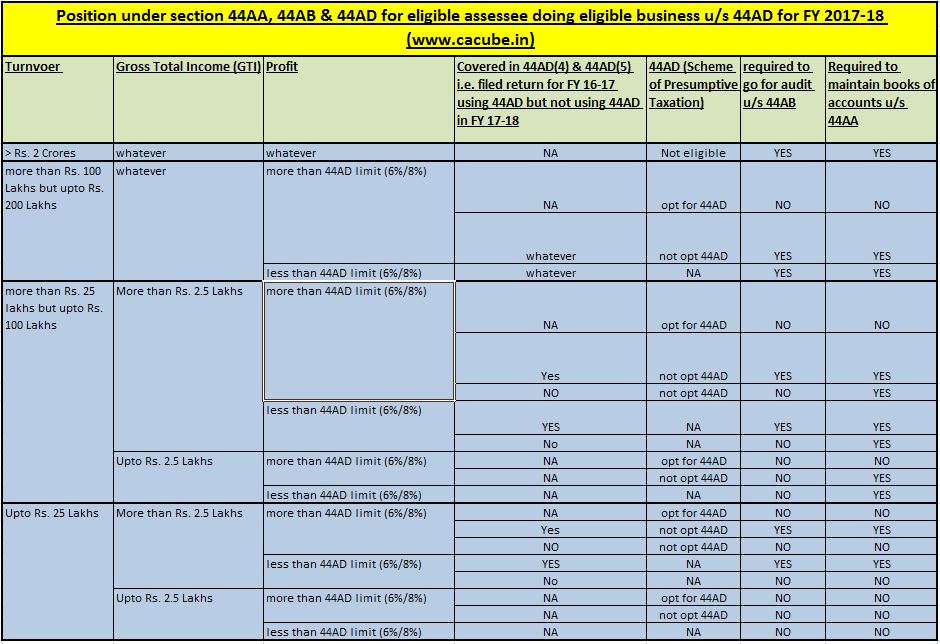

The above answer is drived out from analysis of section 44AA, 44AB and 44AD by comparing position upto FY 2015-16 and after 2015-16 by considering amendment brought in by Finance Act 2016. The summary is analysis is given below:-

Upto FY 2015-16

Till FY 2015-16, eligible assesses having turnover less than Rs 1cr and net profit less than 8% were not allowed to avail the presumptive taxation scheme and had to mandatorily go for tax audit u/s 44AB due to following provisions of law:-

44AB. Every person,—

[(d)

carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section 44AD and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his business and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,]

get his accounts of such previous year audited by an accountant before the specified date and furnish by that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed :

The above section had following three limbs :

- Profits & gains u/s 44AD – Eligible business whose turnover and gross receipts is less than Rs 1 crore

- Claim that such income is lower than the deemed profit i.e. 8%

- income exceeds the limit over which income is taxable

The tax audit for such entities was also supported by Section 44AD(5) as follows :

(5) Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee who claims that his profits and gains from the eligible business are lower than the profits and gains specified in sub-section (1) and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB.

After FY 2015-16

Finance Act, 2016 has brought presumptive taxation to professionals also. The same was incorporated in Section 44AB by replacement of word “business” with “profession”. Post the amendment, the sub-section is as follows :

Section 44AB

44AB. Every person,—

[(d)

carrying on the [profession]shall, if the profits and gains from the [profession]are deemed to be the profits and gains of such person under [section 44ADA] and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his [profession]and his income exceeds the maximum amount which is not chargeable to income-tax in any [previous year; or]]

Therefore, now if business has to come under purview of tax audit, it can come only by way of another sub-section being introduced in the act.

Sub-section ( e) was added to Section 44AB which reads as follows :

44AB. Every person,—

[(e)

carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,]

get his accounts of such previous year audited by an accountant before the specified date and [furnish by] that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed :

So now, audit can only be applicable if provisions of sub0section (4) of Section 44Ad are applicable in case of assesse.

The section 44AD(4) and 44AD(5) ar as follows :

[(4) Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1), he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which the profit has not been declared in accordance with the provisions of sub-section (1).

(5) Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee to whom the provisions of sub-section (4) are applicable and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB.]

As per Section 44AD(4), tax audit will now be applicable only if the following conditions are met

- Assesse declares profit for any previous year (starting from FY 2016-17) in accordance with provisions of 44AD.

- He declares profit for any of the five assessment year succeeding this previous year not in accordance with provision of 44AD as he shows less than 8%/6% profit in the succeeding years.

This is shown by following table:-

I am salaried person and I am doing share trading in F&O. I have loss in F&O business and my income is above basic exemption limit. I have never opted for 44AD. what to do.?

The analysis of section 44AA, 44AB & 44AD is explained very beautifully.

In one line you are not required to go for audit to claim income lower than 8% or 6%. The section which require audit was for such business was 44AB(d) but but this has been amended and w.e.f. FY 2016-17 and new section 44AB(d) is applicable only on profession not business.

Now only if you are covered under section 44AD(4) ie. you have opted 44AD and now opted out of it…to declare lower income then you have to go for audit otherwise not. this is equally applicable from FY 2016-17, FY 2017-18, FY 2018-19 and FY 2019-20 and so on…….see the above table and it is self explaining…